Lloyd’s Strategy: The Oxbow Partners View

1 April, 2026

Lloyd’s five-year strategy 2026-2030

On 19 March, Patrick Tiernan and Rachel Turk set out Lloyd’s new five-year strategy. We view it as a solid if (perhaps necessarily) unexciting strategy after the rollercoaster of Future at Lloyd’s. Patrick Tiernan has recognised the importance of market performance with a clear set of target market KPIs, whilst also acknowledging that he is the steward of a marketplace and not the chief executive of a $58bn insurer. This explains the strategy’s lack of ‘market moonshots’ in favour of fostering an innovation environment for the market’s Members.

The Corporation therefore resumes its role as enabler rather than a disruptor of risk placement. For example, the recent retirement of Blueprint Two is replaced by a refocusing of Velonetic on “incremental technology modernisation, protecting market operational resilience” as part of an ambition to limit the incremental cost of operating at Lloyd’s at 1%.

Management describe the strategy as “market-led with a necessary sharpening of our financial edge,” which we think works well.

As such, the strategy is poles apart from John Neal’s transformational vision, which started as Future at Lloyd’s and transitioned to Blueprint Two. We considered that strategy overly ambitious and unachievable when it was launched and were sceptical about its subsequent roll-out.

Oxbow Partners is supportive of the new strategy, as is much of the market.

What the new Lloyd’s strategy gets right

The Lloyd’s strategy sets six statements for its 2031 ambition:

- Be recognised as the most capital efficient marketplace for complex risk

- Command a share of wallet proportionate to its inherent strengths

- Operate across the full spectrum of commercial and speciality risk

- Be predictable, transparent and investable

- Retain and attract global talent and sophisticated capital as a matter of course

- Sit at the forefront of innovation in underwriting, capital and oversight

We like these statements (which we know from experience are quick to read but take a long time to get right). Lloyd’s has a proud history but its future relevance is not guaranteed in a world where specialty companies are elevating their technical capabilities, expanding their own networks of licences and deploying ever greater capacity.

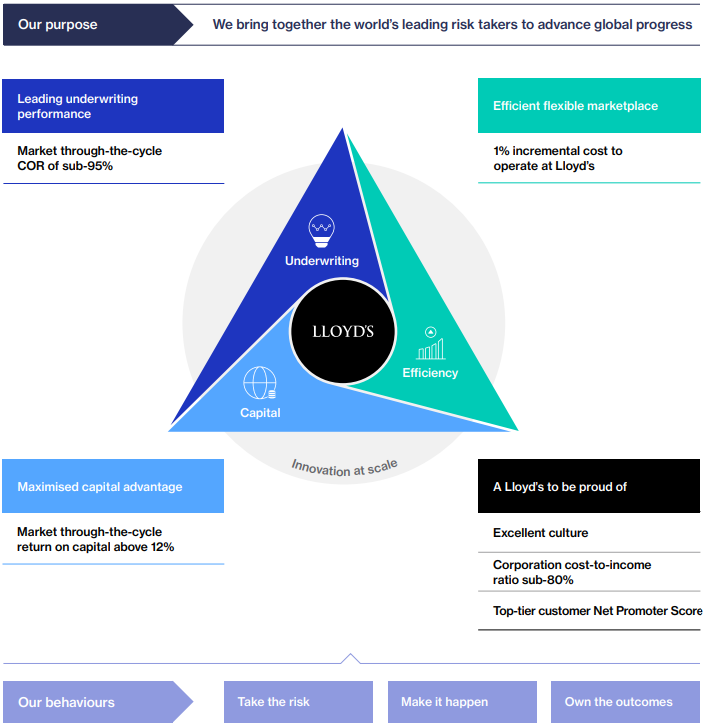

We also like the financial KPIs that Lloyd’s has set as part of its strategy, ensuring a focus on performance over medium- to long-term reform. These are captured nicely in their infographic shown below.

The strategy is built on four pillars

1. Leading underwriting performance

Lloyd’s has done an excellent job since Decile 10 in tidying up its performance, this allowed John Neal to refocus messaging onto growth. Maintaining underwriting discipline will be particularly important in the coming years as pricing softens.

Lloyd’s job in the coming years will be to maintain discipline whilst also being predictable and proportionate. Many market participants complain that expectations shift too often or are hard to read. Clearer signals from the corporation would remove guesswork and help firms plan with more confidence. The current instability in the Gulf will be an early test-case for the market here: how does Lloyd’s answer the call from shipowners and governments for capacity when it is required most, whilst not taking on excessive risk.

2. Efficient and flexible marketplace

This pillar addresses the incremental cost of operating at Lloyd’s. The aim is a market that is simpler to operate, with oversight tailored to different business models – lighter touch where appropriate and sharper focus on material risks. Our understanding is this will go beyond segmentation based on performance and will account for truly different models (e.g. true lead vs. portfolio follow).

After Blueprint Two’s attempts to build a single Lloyd’s tech stack, the new strategy is pushing for an “open architecture ecosystem.” We proposed this shift in our 2019 review of Blueprint One and so welcome the shift now. Lloyd’s should set standards, and participants should then select technology to interact with each other using these standards.

3. Maximised capital advantage

Lloyd’s capital advantage is already substantial for many participants. In our view, Lloyd’s has done an excellent job in recent years establishing itself as a capital marketplace rather than ‘just’ a risk marketplace. London Bridge Two has been a critical part of this, and successes have been several special purpose syndicates set up by major players such as AIG and Allianz to manage their capital stacks.

The strategy sensibly focuses on improving access, not reinventing the model. By reducing friction and simplifying processes, Lloyd’s can make participation easier for both existing and new capital providers. It is an exercise in execution rather than innovation.

4. A Lloyd’s to be proud of

This pillar bundles culture, engagement, data, AI and the Corporation’s own costs.

Progress on culture is tangible: women now hold 35% of leadership roles, up from 29% in 2020, and 93% of boards treat culture as a standing agenda item. Staff sentiment also appears stronger, with 84% of employees willing to recommend their organisation as a great place to work.

The most important signal is the stated intent to listen and respond to Managing Agents and Members. This will mark a break from past perceptions of distance and presumption.

There is also renewed discipline on Lloyd’s own priorities. Cutting ‘extracurricular activities’ makes sense, provided it sharpens capability rather than reducing ambition.

What the strategy is missing

1. Details, details, details

An evergreen comment on a document like this is the lack of detail. In this case, the strategy does not explain how Lloyd’s will cut process and oversight burdens or how it will deliver an ‘open architecture’ within the context of historic technology-related failures or overspend. We would like to understand, for example, where it wants to focus growth or how the segmented operating model will work.

2. Lloyd’s public role

Lloyd’s has a meaningful position in the global specialty marketplace. As such, it should be shaping the environment, not just playing in it. There is little on the role that Lloyd’s will play here and we hope that this is not a retrenchment too far. We have already seen the importance of a strong public relations function in the context of the war in the Gulf.

3. Enhanced underwriting

The majority of market participants have been strategically focused on responding to the rise of enhanced underwriting and the resulting market bifurcation. There is no mention of either in the strategy. You could argue Tiernan’s reference to support for “disciplined portfolio underwriting” is a nod to this, but in our view being silent ignores a key strand in most syndicate strategies.

4. Data and (Gen)AI

Everyone agrees that better data is essential to improve efficiency and effectiveness. Lloyd’s mentions it only briefly, and without a clear sense of intent. Data flows will shape the future of the market, and Lloyd’s should take a leading role. The recent move to fold the chief data officer role into technology does not signal that data is a priority.

What next for Lloyd’s?

It is encouraging to see Lloyd’s go ‘back to basics.’ In 2025 we supported the LMA in articulating Members’ priorities for Lloyd’s and it is good to see many of those themes reflected in the strategy.

The challenge now is delivery. Turning intent into progress will require Lloyd’s to define and answer the next layer of questions and to answer them through a clear, workable delivery model. The market will be wary of anything that drifts back into a sprawling transformation programme. What it will look for instead is ownership, simplicity and a direct line from decisions to outcomes.

The strategy sets a credible direction. Success will hinge on clarity and execution.