Thoughts from the Insurance Insider USA Conference

27 April, 2026

Oxbow Partners attended the Insurance Insider’s New York conference on 23 April 2026. Here are our key take-aways.

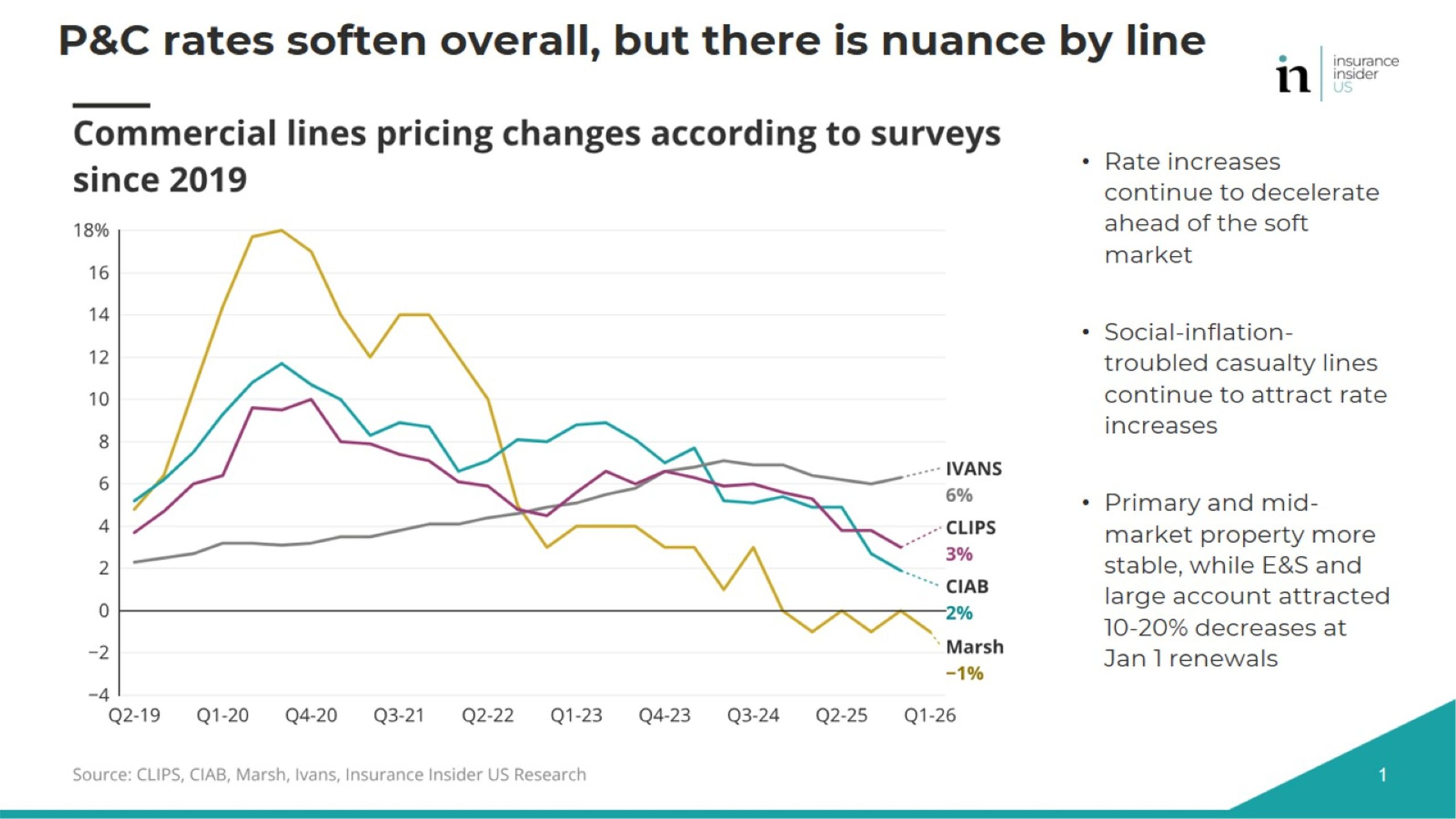

The E&S market is moving “from the Golden Age to the Darwinian age”

Amit Kumar, lead analyst at the Insurance Insider US, led off with an excellent overview about the market (if you don’t read his content, you should!). Amit has been talking about the Golden Age of E&S for some time, but is now referring to the “Darwinian Age” where only the fittest will survive. He noted that “enthusiasm for MGAs” was as high as he could remember.

In Amit’s view, commentary is understating how bad trading conditions are. Every rate indicator is heading solidly south (or, for pedants looking at timeseries data, south east). This sentiment was echoed by execs such as Markel Insurance CEO, Simon Wilson.

In the CEO panel, Emmanuel Clarke from Intact echoed the Darwin analogy. He noted that P&C has the biggest gap between the strongest and weakest performers in financial services, and that the soft market is what sorts the wheat from the chaff. He noted that markets are uneven and that companies need both diversified portfolios and strong analytics to identify where to lean in.

Simon Wilson provided a nice softening market framework in the three Ps – patience, poise and persistence. Companies need to create opportunities and get their timing right in challenging markets, just like athletes or musicians in his analogy.

The Oxbow Partners view is that companies need to ‘play to win’ in this market. Companies who are merely participating will not only trade down with the market, but also incur outsize losses as they are outcompeted by shrewder peers. A clear strategy supported by an operating model that cascades ambition into action is essential.

Scale and (good) M&A are key

Scale is a much talked-about topic as we enter the soft market, and M&A came up in that context of course. However, several panels also noted the strategic importance of M&A to winning strategies – the need for data in the AI age, the ability for scale to attract talent, and a platform that can absorb technology investment costs. The M&A panel got excited by the ‘bifurcation trade’ (think Atrium, Fidelis) as a way to release value. Expect more of these as an example of trades that continue to fragment and re-constitute the value chain.

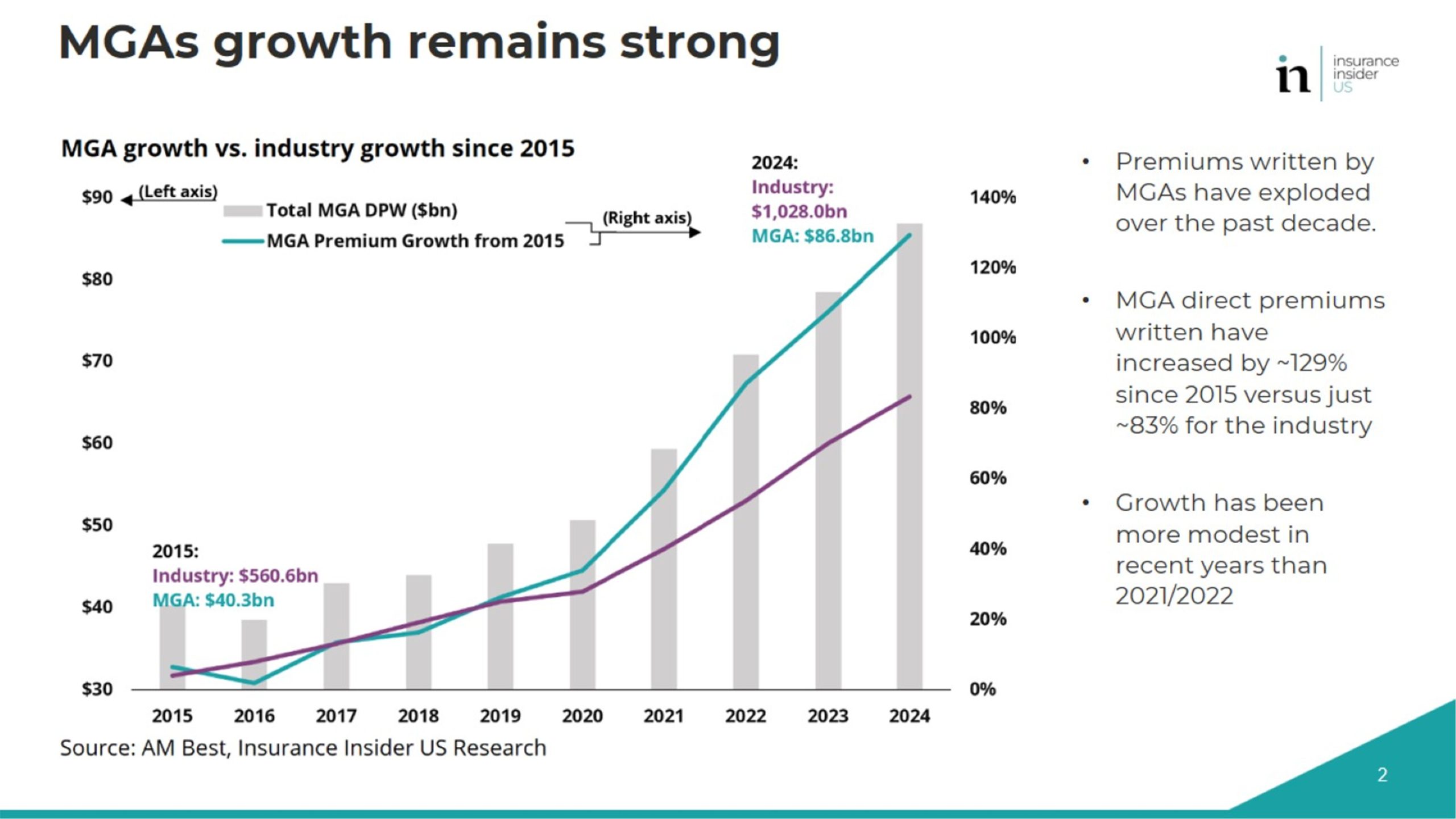

Asked about the biggest risk in the next five years, one panellist noted that it was “poor M&A” – which was echoed by others on the panel. Somewhat tongue-in-cheek, I noted a stark contrast in the data presented by underwriters vs. investors at the conference: whilst underwriters were overwhelmingly bearish, investors generally showed fair-weather charts like the expansion of MGAs.

We observe that most M&A discussions focus on revenue. However, we concur with the panel on the importance of identifying capabilities that you want to source through M&A. Companies need to be clear on their gaps to target state and identify what kinds of company can deliver these capabilities. After all, capability is what gives you ‘edge’, and revenue is an outcome.

AI is critical – obviously

AI featured in almost every panel, whether it was on the agenda or not. One speaker had a nice line that management teams were “moving from fear to fear of missing out”.

Amit Kumar pointed to his research which suggested the margin opportunity: 4-7% for personal lines, 5-9% for commercial underwriters, and 2.5-6.5% for brokers. Greg Williams, CEO of Acrisure, was aligned with these estimates.

AI is currently a “workflow and margin” lever, as Amit described it, a view supported by all speakers. It was interesting that no speakers suggested that AI was going to fundamentally change the way companies were structured and operated. The Oxbow Partners view is that the leading adopters of AI will re-organise around capabilities, with AI taking care of the foundational data gathering and analysis processes and people contextualising those outcomes, applying judgement and using them in relationships. We will be publishing further on this soon.

(You may be pleased or disappointed to hear that this note was written by a human based on handwritten notes.)

Exposure is challenging

There were a couple of interesting anecdotes about risk. Emmanuel Clarke from Intact noted that the risk environment is becoming ever more connected and that achieving true diversification was increasingly hard. AI will only accelerate this trend. Another nod towards scale.

InsurTech dying, long live FinTech

We observe an interesting shift in the definition of ‘InsurTech’. Startups have been keen to drop this label in recent years as the class has struggled. On the other hand, Greg Williams from Acrisure – a c.$5bn platform – called his business a “global AI-driven Fintech platform”. It is interesting how Fintech is still considered ‘valuation accretive’ whilst InsurTech is not.

Whilst we’re on Acrisure, Greg’s story was fascinating. The company has made around 1,000 acquisitions in the last 12 years and posted compound annual growth of 45% since then. It has an AI platform that gives agents advice on next best actions, but Greg noted the criticality of humans in the sales process.

The company has invested in a payroll company and now sells non-insurance products to clients. Interestingly, the company tested this idea by initially targeting 1,000 clients and selling leads to payroll companies. When it achieved a take-up rate of 55% on that sample, it knew it was time to buy a company. When you test ideas like this, you earn the right to call yourself a Fintech!

The overall take-away is that challenging conditions are ahead, but there was optimism amongst some that challenges also lead to opportunities. But nobody seemed more bullish than the lawyer and bankers on the M&A panel.

About the author

Chris Sandilands is a Partner at Oxbow Partners.