About the author

Oxbow Webmaster

Oxbow Partners is an advisory firm exclusively serving the insurance industry.

Contact OxbowGet market insights straight to your inbox

Keep me informed

December 2, 2016 Oxbow Webmaster

Machine learning, artificial intelligence (see this blog for a primer) and other analytical techniques are hot topics in insurance at the moment. However, the hype has not so far translated into many actual implementations. In this guest blog, AI specialist Edwin Chung and actuary Wayne Chen, members of the Oxbow Partners Expert Network, discuss how their experiences in the retail industry could help insurers radically improve their understanding of customers – and therefore drive financial performance.

When Dunnhumby helped Tesco introduce its Club Card in 1994, Tesco’s then-Chairman Lord MacLaurin commented: “What scares me about this is that you know more about my customers after three months than I know after 30 years.” That was 22 years ago.

It was therefore with some surprise that we discovered in a recent conversation with Oxbow Partners that some insurers and brokers have little in the way of customer analytics and segmentation.

Much has changed since Tesco introduced the Club Card. The techniques used by Dunnhumby in 1994 can now be considered part of the analytical stone age. Retailers are building increasingly precise pictures of their customers – remember the story of US retailer Target knowing a lady was pregnant before she did? – and delivering increasingly specific marketing messages and propositions as a result.

In this blog we share some of the thinking that retailers are spearheading and consider how it could be applied to insurers.

Machine learning is the process by which computers get more intelligent without explicit programming. When you search for something on Google, for example, Google’s machine learning ingests data about your habits and automatically updates its ranking system for future searches. In other words, machine learning is a way that computers build up artificial intelligence.

Many retailers have access to an unfathomable amount of intelligence about their customers. This is not limited to structured data such as till data: consider, for example, that natural language processing – another AI technique – can now ingest and understand data sources such as prose and increasingly speech. (Ever wondered why Google offers voice-based products? This article suggests that it’s to help them build their voice processing algorithms.)

This breadth and depth of data cannot be processed by humans with spreadsheets.

Machine learning applications can, however, collect, organise and analyse the data. Customer insight professionals can continuously enhance their understanding of each customer.

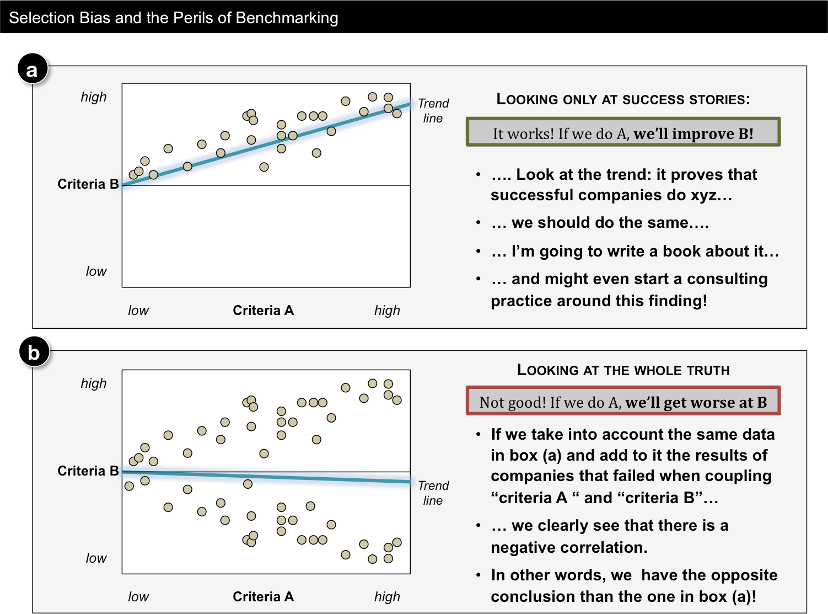

This level of insight allows companies to make better decisions. As the illustration below shows, using limited data sets can sometimes lead to false conclusions. Machine learning allows companies to look at more data and perform analysis in more dimensions.

Machine learning allows companies to do two things.

First, it allows them to identify the most predictive signals for their customers. In the old world, retailers used signals like post code and age and abstracted this to personas. In the new world, retailers can use more subtle signals, and in particular combinations of signals, to cluster customers into segments. So, for example, as you add new customers, your machine learning algorithms might tell you that a new characteristic is becoming a more dominant signal in your data.

Second, retailers can build more dynamic clusters. As behaviour changes, retailers can update their segmentations to keep track of customer demand. This is often described as “adaptive segmentation”.

These two things work in combination and are additive. Every modern retailer is on a journey to refine their customer segmentation, and none will ever arrive. However, on the journey they are all able to adapt their marketing messages and proposition to their customers.

There are a number of challenges for insurers and brokers in implementing machine learning and other forms of data science. The most pressing is a lack of data or fragmented legacy data spread across the organisation. (As Oxbow Partners point out in this blog, many management teams only monitor financial data and not behavioural data. This is not helpful for customer segmentation.)

The first step to implementing machine learning is, therefore, a cultural change. Insurers and brokers need, over time, to collect as much data about their customers as possible and build a data infrastructure to warehouse and analyse it. This is not a trivial task and retailers have invested heavily in doing this. It is important that management commit to this vision otherwise further effort will be wasted.

An element of the cultural change is the respective roles of actuaries and data scientists for insurers. Data scientists are specialists in complex analysis of often unstructured data. This is different to the kind of analysis in which actuaries are skilled. Certain functions will benefit from the cooperation of the two teams, for example reserving. Insurers will need to develop structures to encourage the cooperation of these teams.

Second, insurers and brokers need to embed analytics capability into their organisations. Contrary to what many think, machine learning is not a piece of software that can be implemented and left to its own devices. Instead, it is a tool that data scientists can use. True AI which runs a business in its own do not yet exist; algorithms still need to be pointed in the right direction with human insight, hypotheses and data sources. You cannot launch a machine learning enabled segmentation exercise until you know what you’re looking for.

We have helped several retailers improve their customer segmentation. In one case, for example, this led to the retailer discovering that they had only a 20% share of wallet for even their best customers. The retailer was able to launch a number of initiatives to target these customers more actively.

We believe that there is a huge opportunity for insurers and brokers to learn from other industries such as retail.

As a first step, we recommend a diagnostic phase where we assess your data infrastructure readiness and support you outline your objectives and set up hypotheses for your analysis.

From here we can then begin to build out your analytics programme. We strongly believe that any company is capable of implementing machine learning. However, it takes time to create the right data infrastructure and identify your resource needs and recruit those people. During this set-up phase we support companies build the initial infrastructure, perform initial analysis (for example by translating human hypotheses into code) and set up a transition plan to a permanent team. Oxbow Partners call this approach to building businesses and functions Agile Strategy™.

For more information, please contact the Oxbow Partners team.

Get market insights straight to your inbox

About the author

Oxbow Webmaster

Oxbow Partners is an advisory firm exclusively serving the insurance industry.

Contact Oxbow